Are You Ready for Tax Bracket Madness?

Posted in Category: Taxes

Tagged with : Taxes

Basketball and Taxes

Here’s a random thought, unless you’re a pro basketball player, you’ll probably never think of basketball and taxes together. But in a strange way, the two worlds collide in March for hoops fans and tax filers alike.

Basketball, because of March Madness buzzer beaters and bracket busters. Taxes, because of filing deadlines and federal income tax brackets.

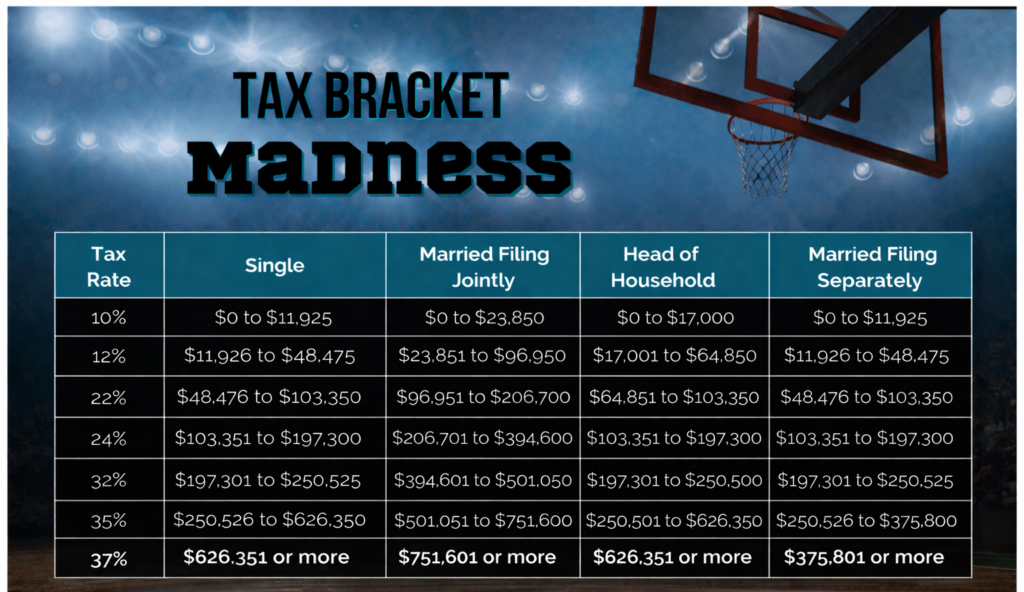

And whether you’re a basketball fan or not, understanding tax brackets is a game we all need to play. To illustrate how this game works, imagine your taxable income as a team playing in the ultimate tax tournament. Let’s start with reviewing the federal income brackets for 2025 tax returns and play through two different scenarios.

Love and Basketball

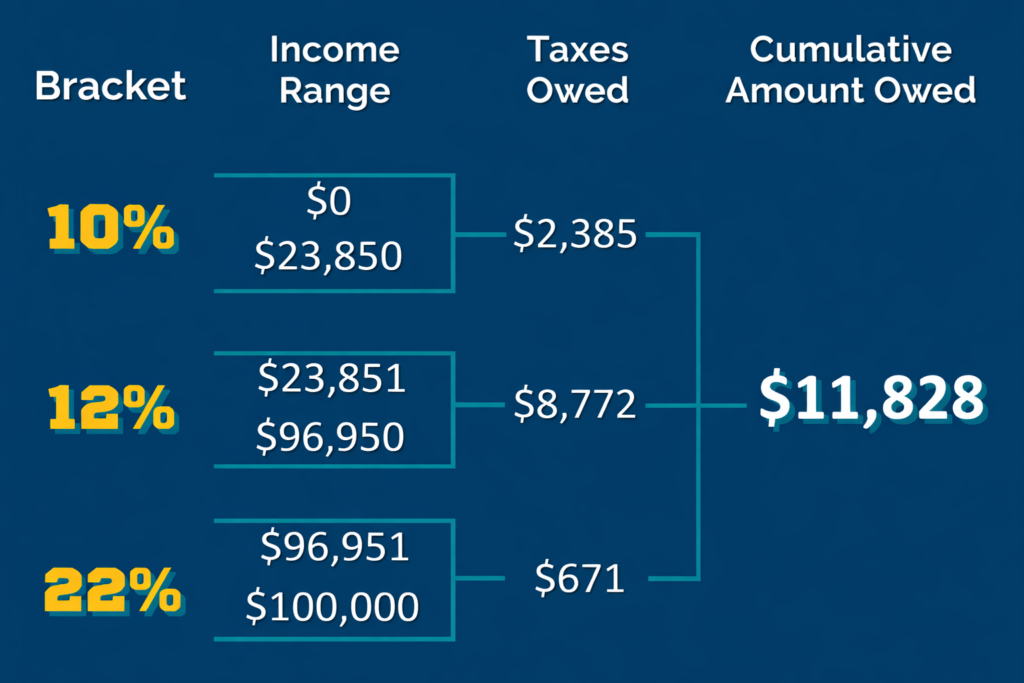

Suppose newlyweds Quincy and Monica have taxable income of $100,000 this year and file their taxes jointly. According to the chart shown above, it might feel like a slam dunk to assume they are taxed 22% on the full amount and will face a tax liability of $22,000. However, this game is played with a little more nuance.

Here is how the $100,000 is taxed as this couple advances through several tax brackets.

10% Bracket: The first $23,850 they earn is taxed at 10%, and results in $2,385 of taxes due from this bracket.

10% Bracket: The first $23,850 they earn is taxed at 10%, and results in $2,385 of taxes due from this bracket.- 12% Bracket: The dollars earned from $23,851 to $96,950, face a 12% tax, adding up to $8,772 due from this bracket.

- 22% Bracket: The dollars they earn over $96,951 triggers a 22% tax and results in a total liability of $671 for this bracket.

So, let’s tally the results for these newlyweds. Quincy and Monica advance through three tax brackets, spreading their dollars around the court, and incur a tax liability of $11,828 or 11.8%.

This amount is significantly less than the 22% we originally assumed.

Single and Ballin’ Out

Suppose Duke is single and “ballin’” in more ways than basketball. H

is taxable income is $180,000 this year, landing him firmly in the 24% bracket. But as with the previous example, things are not as obvious as they might seem.

Here is how the $180,00 is taxed as Duke advances through several tax brackets.

10% Bracket: The initial $11,925 is taxed at 10%, for a total of $1,193 in this bracket.

10% Bracket: The initial $11,925 is taxed at 10%, for a total of $1,193 in this bracket.- 12% Bracket: From $11,926 to $48,475 his team faces a 12% tax, adding up to $4,386 for this bracket.

- 22% Bracket: Advancing to the next bracket, means the dollars earned from $48,476 to $103,350 will trigger a 22% tax, adding up to $12,072 for this bracket.

- 24% Bracket: The final dollars earned above $103,351 are taxed at 24%, adding up to $18,396 owed from this bracket.

For those scoring at home, Duke advances through four tax brackets and incurs a potential tax liability of $36,047 or approximately 20% of taxable income.

This amount is less than the 24% we originally assumed.

Cut Down the Nets

While I only shared examples for single and married (filing jointly) taxpayers, the logic and approach work the same for Married Filing Separately and Head of Household. The numbers are just different.

It’s also important to understand that the information presented in this blog is not to be taken as tax advice and everyone’s situation is different. We’re just trying to help you understand how the brackets work.

If you need an assist in completing your tax return this year, MilTax offers free software and support to ensure your tax return is a winner.

The USAA Educational Foundation is a nonprofit, tax-exempt IRS 501(c)(3) and cannot endorse or promote any commercial supplier, product, or service. The content of this blog is intended for information purposes only and does not constitute legal, tax, or financial advice.